Analyst Recommendations On State Bank Of India

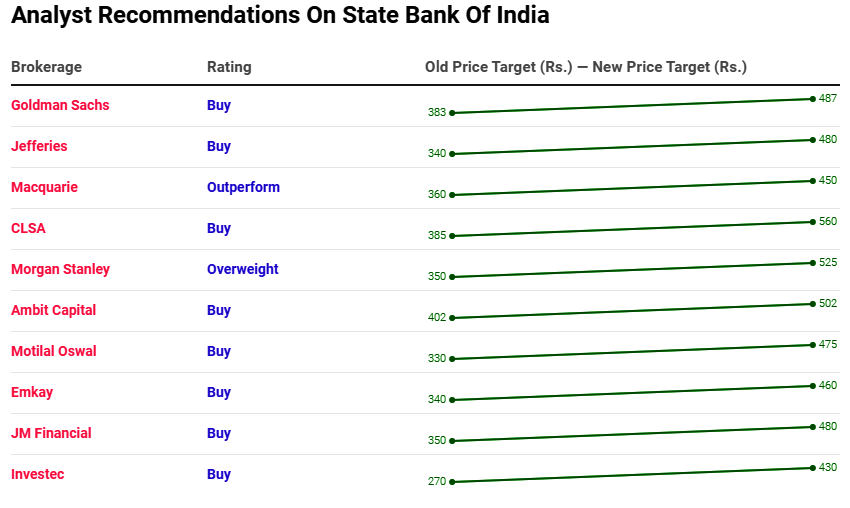

- Maintains ‘buy’ rating; raises price target to Rs 560 apiece from Rs 385.

- Strong NII provision; large buffer built for employee provisioning.

- Asset quality is delivering better outcomes versus even private banks.

- Revises earnings estimates higher by 15-26% and expects RoEs of 14% by FY23.

- Expects material re-rating beyond 1x book.

- Still remains a deep value opportunity and current re-rating should continue.