Analyst Recommendations On State Bank Of India

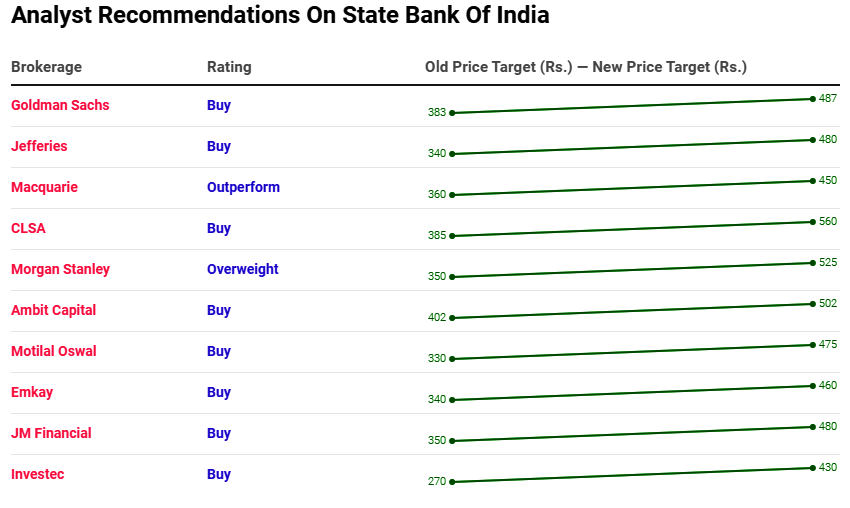

- Maintains ‘buy’ rating; raises price target to Rs 560 apiece from Rs 385.

- Strong NII provision; large buffer built for employee provisioning.

- Asset quality is delivering better outcomes versus even private banks.

- Revises earnings estimates higher by 15-26% and expects RoEs of 14% by FY23.

- Expects material re-rating beyond 1x book.

- Still remains a deep value opportunity and current re-rating should continue.

Macquarie

- Maintains ‘outperform’ rating; hikes price target to Rs 450 apiece from Rs 360.

- Increased confidence in balance sheet, strong asset quality.

- Pare credit cost assumptions for FY21, FY22 and FY23 by 40, 30 and 30 basis points, respectively, to 240 basis points, 120 basis points and 120 basis points.

- Can sustain RoA of 1%.

- Raises EPS estimates by 77%, 13% and 14% for FY21, FY22 and FY23, respectively.

- Remains top pick among PSUs.

JM Financial

- Maintains ‘buy’ rating; raises price target to Rs 480 apiece from Rs 350.

- Strong results with improvement across all key parameters.

- Expects SBI to report lower slippages / restructuring for FY21, followed by sharp declines in FY22/FY23.

- Liability franchise remains unparalled with deposit growth of 14% and robust CASA ratio.

- Asset quality perceptions kept valuations suppressed despite core fundamentals consistently outperforming.

- Expects RoA/RoE of 0.8% and 15%, respectively, by FY23 as credit costs normalise.

- Expects multiples to re-rate higher as RoAs expand.

- Remains top pick.

Emkay

- Maintains ‘buy’ rating; hikes price target to Rs 460 apiece from Rs 340.

- Once again surprised positively on asset quality.

- Retail credit growth gaining pace which should lead to structurally stronger NIMs.

- Will be one of the biggest beneficiaries of the pick-up in lumpy corporate resolutions stalled for long.

- Revises earnings estimates higher for FY21-23 by 30-60% and expects RoAs and RoEs of 0.8% and 14%, respectively, in FY23.

- Limited stress from Covid, corporate resolutions to drive-down credit costs.

- Likes strong liability profile, higher retail orientation and sharply improving return ratios.

Motilal Oswal

- Maintains ‘buy’ rating; raises price target to Rs 475 apiece from Rs 330.

- Robust operating performance in a challenging environment.

- Asset quality outlook encouraging.

- Slippages plus restructuring to remain within the guided range.

- Strong operating performance, controlled slippages and higher coverage provides comfort.

- Well on track to keep credit costs under control.

- Recoveries from resolution of large accounts can further support earnings.

- Projects RoA, RoE of 0.8% and 14.5% by FY23.