Gold Silver Reports – In anticipation of strong results for the September quarter, Larsen and Toubro Ltd’s (L&T’s) stock closed 4% higher on Friday. The Street was not wrong, and the diversified conglomerate’s operating performance easily beat estimates.

But the huge negative surprise that could puncture investor confidence in the near term was a sharp cutback in full-year (FY18) order flow guidance to zero, from about 12% pegged at the beginning of the year.

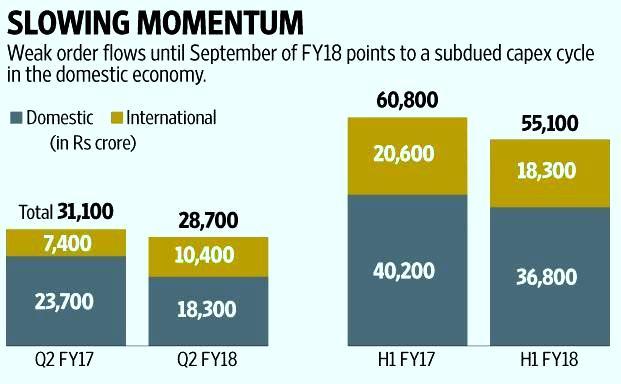

Normally, the management has held back any changes in guidance until the December quarter. This fiscal year, the June and September quarter order flows were both lower by 11% and 8% year-on-year (y-o-y), respectively.

This U-turn in forecast underscores the sluggishness in the domestic economy.

L&T’s pessimism stems from the consistent delays witnessed in the time taken for translation of an opportunity into an order in large infrastructure projects.

Adding to the misery now is the impact of demonetisation and the goods and services tax (GST) that have slowed growth rates and hurt small contractors.

A wary banking system is another reason for delays in financial closures of large infrastructure projects.

Not surprisingly, L&T’s order book growth, which may be taken as a proxy for the country’s economic health, inched up by only 2% in 12 months. Two-fifths of this comprises international orders.

Fortunately, L&T’s sizeable order backlog of Rs2.6 lakh crore built over the previous years will keep revenues ticking. The management has, therefore, retained its revenue guidance at 12% for FY18.

However, GST-led issues restrained the pace of execution and the quarter’s revenue rose by 6% y-o-y to Rs26,446.8 crore, slightly lower than Bloomberg’s estimates. Here again, the infrastructure segment that comprises about 44% of the total revenue grew by a paltry 2%, as delays in clearances still haunt the sector. Revenue got a leg-up from the information technology and financial services sector.

That said, in challenging times, L&T’s resilience, with stringent working capital management and cost control, is commendable. The quarter’s operating profit rose by 28% to Rs2,960 crore, with a significant contribution from developmental projects. With all segments firing well, operating margin at 11.2% was 190 basis points higher than the year-ago period and equally higher than the 14-broker estimate by Bloomberg. One basis point is one-hundredth of a percentage point.

Read More: Fear of Revenue Loss Abates as GST Collections Gain Momentum

Net profit, after adjusting for an exceptional gain on divestment of a subsidiary was 17.3% higher at Rs1,683 crore, beating the forecast by 38%. The stellar performance is already discounted by L&T’s stock that trades at Rs1,264, discounting FY19 earnings a fair 20 times.

But the crucial thing to watch for in the coming week is whether a huge reduction in order inflow growth will dampen investor exuberance.

Also, in the coming quarters, the Hyderabad Metro project, once flagged off, will weigh on earnings, as interest costs and depreciation from the project will be accounted for. So far, L&T has deftly managed its finances. Its keenness to proceed on InvITs (investment trusts) indicated the intent to move some infrastructure projects off its books. This would lower interest costs to accelerate earnings growth. – Neal Bhai Reports